Research Areas

New Research

Tax Compliance

Covid Policy

Income Inequality

Tax Progressivity

Income Mobility

Tax Credits/Policy

Health/Pensions

Curriculum Vitae

Google Scholar

For the Internal Revenue Service, marriage is less about romance and more about a change in filing status.

But some couples pay more in taxes as a married pair than they would as individuals.

These tax increases are called marriage penalties.

To address the problem of misreported marriage statuses, we link two sets of administrative data: state marriage records and federal tax returns.

We find that taxpayers are sensitive to the financial impacts of marriage penalties.

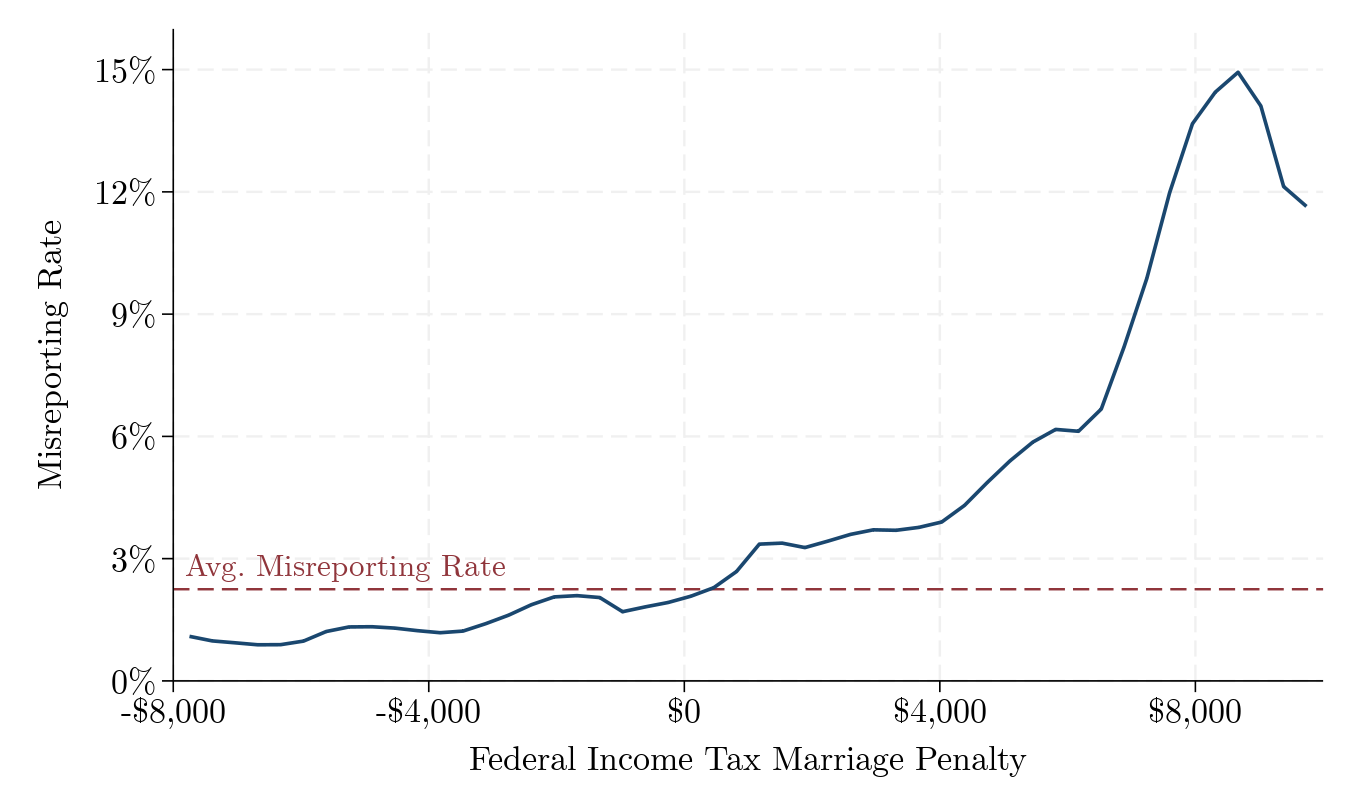

Figure 1: Marital-status misreporting and marriage penalties among newlyweds, 2001-2022

Do Marriage Tax Penalties Cause Delayed Marriage Reporting? (summary)

March 2026 (full paper, pdf)

Prior studies showed marriage penalties have little effect on marriage decisions, as most couples don't stay single to reduce taxes.

Still, couples can have their (wedding) cake and eat it too; get married but then don't tell the tax authority.

In Gorman and Splinter (2026)

, we use administrative data to reveal that while taxes might not stop the wedding, they may stop the reporting of the marriage.

Finding Newlyweds Who Misreport

Starting with about half a million marriage records from Minnesota, a state with accessible public marriage records, we match newlyweds to their tax returns.

As we don't observe divorces, we focus on newlywed couples who delay reporting their marriage to the IRS.

This allows us to see the "true" (based on legal marriage certificates) versus the "reported" marriage status on tax returns.

This shows a group of misreporters: couples who are legally wed but continue to file as unmarried after their marriage.

Marriage Misreporting Increases with Marriage Penalties

The figure below shows the relationship between misreporting rates and penalty amounts. Newlyweds with a tax marriage bonus misreport at a rate of only 1.5%. These couples would pay less in taxes (or get more credits) by reporting their marriage, suggesting they misreport due to inattention to tax incentives or filing requirements.

As the penalty increases, however, so does the rate of marital-status misreporting. For couples facing a $4,000 penalty, the misreporting rate jumps to 4%. At an $8,000 penalty, the misreporting rate reaches 14%.

Once the penalty hits the $8,500 mark—roughly the maximum marriage penalty from the Earned Income Tax Credit (EITC)—the misreporting rate begins to level off, suggesting the EITC contributes to this noncompliance behavior.

Misreporting isn't only a one-time error. These misreporters wait an average of two years before they report their marriage to the IRS. Why do they eventually report their marriage? We track couples over time and find they often start reporting their marriage the exact moment their marriage penalty turned into a marriage bonus.

Marriage vs. EITC

Marriage penalties can be quite substantial among certain groups, especially couples where both spouses work and they have more equal earnings.

Marriage penalties can also be large for those with children who claim the EITC.

The EITC is the nation' largest anti-poverty program for workers. The credit therefore phases out as income rises. When low-income or middle-income earners marry,

however, their combined earnings can push them into the phase-out range and decrease their credits.

Consider a couple with three children where each spouse earns $20,000. If they file separately, they have a combined $10,000 in tax credits.

If they file a joint return as a married couple, that credit drops to about $4,000. The marriage penalty is the difference: $6,000,

or nearly 15% of their total household income. This creates an incentive for certain newlyweds to delay reporting their marriage to the IRS.

For EITC-only marriage penalties (as compared to total penalties), we observe the same pattern of misreporting as the figure above.

Policy Implications

What does this mean for the $7 billion that the IRS estimates it loses every year due to filing-status errors?

The U.S. is an outlier in how it handles the reporting of marriages. In 85% of OECD countries, the government uses marriage registries to pre-fill

tax returns with the correct marriage status. In contrast, the U.S. lacks a national marriage registry and so relies on an honor system of self-reporting.

This could be addressed with better information sharing. If the IRS could automatically match returns against state marriage and divorce records,

it could identify incorrect filings.

Gorman and Splinter (2026) show that incentives matter. People still follow their hearts to the altar, but some follow their wallets when it's time to file a tax return.

Read the full paper here (pdf).